Crypto Taxes for Beginners: The Simple Guide to Avoid Costly Mistakes

Taxes & Rules: The Most Common Fear for New Crypto Users

You might think the biggest fear for new crypto users is losing money in a market dip. Actually, for many beginners, the prospect of a tax mess is far more terrifying than a price drop.

Why? Because market volatility feels like a force of nature. Tax mistakes, on the other hand, feel like a personal failure with real financial penalties. This anxiety is widespread. A survey in 2026 found that only 49% of crypto users correctly understood a core tax rule, revealing a massive knowledge gap. Another study from the same year by a major exchange confirmed it, showing that half of crypto investors are unaware of their basic tax obligations.

The confusion often starts with one simple question: Am I trading or investing? Getting this wrong has real consequences.

- If you buy and sell crypto quickly, you’re likely trading. This means any profit you make could be subject to a higher crypto short term capital gains tax.

- If you buy and hold for over a year, you’re investing for the long term. Your long term crypto tax rate is generally much lower

and can significantly increase your final returns.

Not knowing this difference is more than just a paperwork headache. It can lead to unexpected tax bills that eat into your profits.

This fear of getting the rules wrong is also deeply connected to another major worry: choosing a safe place to buy and hold your crypto. When you don’t understand the crypto market structure bill or other regulations, how can you judge which platforms are secure and legitimate? Scams and unstable platforms prey on this exact confusion.

The good news is you don’t need to become a tax attorney. You just need clear, simple steps to build a solid foundation. Start by learning how to trade Bitcoin safely and always use a safety-first checklist before trusting any platform with your money.

To cut through the complexity and get step-by-step guidance delivered in plain English, many beginners find it helpful to subscribe to free educational newsletters like Clicks and Trades. Getting clear information is the first step to turning fear into confidence.

Ready to make sense of crypto taxes and safety? Sign Up for straightforward tips and guidance to help you start on the right foot.

Crypto Tax 101: What the IRS and Other Authorities Actually See

Let’s start with the single most important rule you need to know. In the eyes of the IRS, your cryptocurrency is treated as property, not as regular money. This was established way back in 2014 and remains true in 2026. Think of your Bitcoin or Ethereum like a stock or a piece of real estate you own.

This "property" rule is the key that unlocks the entire tax picture. According to IRS guidance, because crypto is property, any time you sell, trade, or spend it, you are creating a taxable event that must be reported. This means you owe taxes on your capital gains, which is just a fancy term for the profit you made.

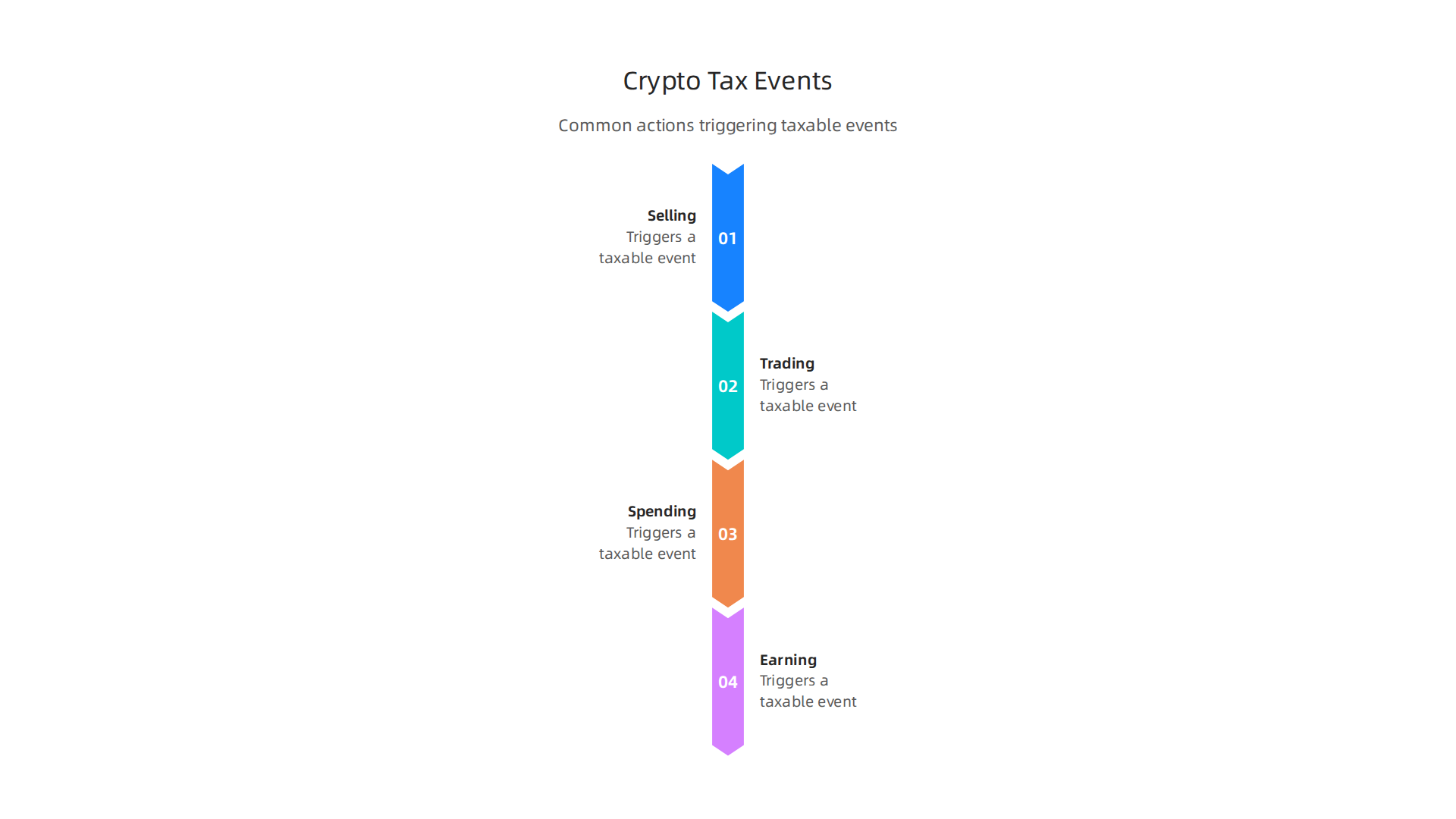

So, when do you trigger a taxable event? Here are the most common situations:

- Selling Crypto for Cash: This is the most straightforward event. If you buy 1 Bitcoin for $50,000 and later sell it for $70,000, you have a $20,000 capital gain that is subject to tax.

- Trading One Crypto for Another: This is a big one many people miss. If you trade your Ethereum for Solana, the IRS sees this as you selling your Ethereum (creating a taxable gain or loss) and then buying Solana with the proceeds. You must calculate the value of your Ethereum at the moment of the trade.

- Spending Crypto: Using crypto to buy a laptop, pay for a service, or make a donation is treated as selling it. You need to figure out if the crypto’s value went up or down since you originally got it.

- Earning Crypto: Receiving crypto as payment for work, as a reward from staking, or from an airdrop is typically treated as ordinary income. You pay income tax on its fair market value on the day you receive it. You can see how platforms will now report many of these transactions on the new Form 1099-DA.

Now, here’s the great news that removes a lot of fear: Simply buying and holding cryptocurrency in your own wallet is NOT a taxable event. The IRS does not tax you for owning an asset that increases in value. You only owe tax when you "realize" the gain by selling, trading, or spending it. This principle is why understanding your long term crypto tax rate is so powerful for investors.

The length of time you hold before selling makes a huge difference. As noted in the IRS instructions, if you hold for one year or less, your profit is a crypto short term capital gains tax and is taxed at your regular income tax rate, which can be high. If you hold for more than one year, you qualify for the lower long term crypto tax rates, which can save you a significant amount of money. This "holding period" rule is a cornerstone of tax planning, as highlighted in recent advisory reports.

While these are the core IRS rules, it’s wise to keep an eye on legislative changes, like discussions around a potential crypto market structure bill, which could influence reporting and definitions in the future. The most important thing you can do right now is build your knowledge on a solid foundation. Before you even make your first trade, ensure you know how to trade Bitcoin safely using a clear checklist.

Taxes don’t have to be a scary mystery. With clear rules, you can plan confidently. For straightforward explanations and step-by-step guides delivered to your inbox, many beginners rely on the free Clicks and Trades newsletter. It breaks down topics like this into plain English, helping you stay informed without the overwhelm.

Ready to build your crypto knowledge with clear, simple lessons? Sign Up for the free Clicks and Trades newsletter to get helpful tips and guidance sent directly to you.

Short-Term vs. Long-Term Capital Gains: The Huge Difference for Your Crypto

You now know that selling or trading your crypto is a taxable event. But here is where many new investors get tripped up. The tax you pay isn’t just one flat rate. It changes dramatically based on one simple thing: how long you held the crypto before you sold it.

This is the difference between short-term and long-term capital gains. Understanding this is the key to smart crypto tax planning.

The Holding Period Clock: When Does It Start?

First, you need to know how to measure your "holding period." The IRS is very specific about this.

The clock starts ticking the day after you acquire the cryptocurrency. You count every day you own it, right up to and including the day you sell or trade it away.

According to the IRS instructions for Form 8949, which is where you report these sales, a short-term holding period is generally one year or less. A long-term holding period is more than one year.

Think of it like this simple timeline:

Day 1: You acquire 1 Bitcoin.

Day 365: You have held it for exactly one year. This is still considered a short-term holding.

Day 366 and beyond: Congratulations. You have now entered the territory of long term crypto tax treatment.

Why the One-Year Mark is a Financial Fork in the Road

This one-year threshold is critical because it determines your tax rate. The difference in what you owe can be substantial.

-

Crypto Short Term Capital Gains Tax: If you sell an asset you’ve held for one year or less, any profit is taxed as short-term capital gains. This profit is simply added to your total annual income and taxed at your ordinary income tax rate. For most people, these rates are 10%, 12%, 22%, 24%, 32%, 35%, or 37%. They can get quite high.

-

Long Term Crypto Tax Rates: If you hold your crypto for more than one year, your profit qualifies as a long-term capital gain. These gains are taxed at special, reduced rates. As of 2026, the long-term capital gains rates are typically 0%, 15%, or 20%. Which rate you pay depends on your total taxable income, but they are almost always lower than your ordinary income rate.

Let’s look at a real example from a tax analysis. A report from KPMG on digital asset legislation illustrated a case where an investor’s long-term gain was taxed at a 20% rate, highlighting the potential tax savings from patient investing. You can see similar analyses in global reports, like the PwC Annual Global Crypto Tax Report, which examines how different countries treat holding periods.

What This Means for Your Investment Strategy

The math is compelling. Holding for over a year can put thousands of dollars back in your pocket.

Imagine you bought Ethereum and it increased in value by $10,000.

- If you sold after 11 months, that $10,000 gain could be taxed at, say, 24% (your income tax rate). You’d owe $2,400 in taxes.

- If you waited just one more month to pass the one-year mark, that same $10,000 could be taxed at the long-term rate of 15%. You’d owe only $1,500 in taxes.

By being patient, you just saved $900. This principle is why "buy and hold" isn’t just an investment mantra. It’s a powerful tax strategy.

This foundational rule of property treatment, where "gains/losses follow capital rules; holding period matters," as outlined in crypto tax guides, is your best tool for planning. It’s also wise to stay informed about broader regulatory changes, like discussions surrounding a potential crypto market structure bill, as future laws could refine these rules.

Planning your trades with the tax timeline in mind is a cornerstone of responsible investing. Before you make a move, having a solid plan is crucial. For a clear, step-by-step approach, review this beginners checklist for how to trade Bitcoin safely.

Keeping up with these details doesn’t have to be a solo job. For straightforward lessons on topics like taxes, security, and strategy, many investors find it helpful to follow a simple, free newsletter. Clicks and Trades delivers clear, step-by-step crypto education to help you make confident decisions.

Ready to make smarter, more informed crypto decisions? Sign Up for the free Clicks and Trades newsletter to get helpful tips and guidance sent directly to you.

Step-by-Step: How to Actually Calculate Your Crypto Taxes

You know the big difference between short-term and long-term capital gains. Now, it’s time to get practical. How do you actually figure out what you owe? It’s not as scary as it sounds if you break it down into simple steps.

Step 1: Gather Your Transaction Records

This is the most important step. You cannot calculate your taxes without all the data.

Go to every exchange and platform where you bought, sold, traded, or earned crypto. Download a complete transaction history for the entire tax year. Look for a report called a “Transaction History,” “Tax Report,” or “Capital Gains Report.” You’ll need details like:

- The date and time of each trade

- The type of transaction (buy, sell, trade)

- The amount of crypto involved

- The value in your local currency (like USD) at the time of the transaction

- Any fees you paid

If you use a non-custodial wallet (one where you control the keys), you’ll need to track those transactions too. Starting with a solid foundation is key, so if you’re new, reviewing a guide on common mistakes to avoid with a non-crypto wallet first can save you headaches later.

Step 2: Understand Your “Cost Basis”

This is the core of the calculation. Your cost basis is simply what you originally paid for your crypto, including any fees. It’s your starting point for figuring out profit or loss.

When you sell, you need to match the sold crypto with the specific lot you bought to determine its cost. The IRS allows different methods to do this matching, and your choice can change your tax bill. A detailed guide on what a crypto calculator does and doesn’t do can help you understand how these tools use your data.

Here’s a quick look at the common methods, as outlined in resources from firms like Koinly and CoinTracker:

| Method | How It Works | Best For… |

|---|---|---|

| FIFO (First-In, First-Out) | Sells the oldest coins in your portfolio first. | Simplicity; often the default for taxes. |

| LIFO (Last-In, First-Out) | Sells the most recently acquired coins first. | Potentially lowering gains if newer coins cost more. |

| HIFO (Highest-In, First-Out) | Sells the coins with the highest purchase price first. | Minimizing taxable gains in the current year. |

| Specific Identification | You choose exactly which lot of coins you are selling. | Maximum control for tax strategy. |

Most experts recommend checking if HIFO is allowed for your situation, as it can legally minimize your current year’s tax. As noted by tax professionals, choosing the right crypto cost basis method is a key strategic decision.

Step 3: Walk Through a Simple Calculation

Let’s use a straightforward buy-and-hold example to see the math in action.

The Scenario:

- January 15, 2025: You buy 1 Bitcoin (BTC) for $40,000. You pay a $50 trading fee.

- Your Cost Basis: $40,000 + $50 = $40,050.

- February 20, 2026: You sell your 1 BTC for $60,000, paying a $60 network fee.

Step A: Find Your Proceeds.

Sale Price minus Sale Fees: $60,000 – $60 = $59,940.

Step B: Calculate Your Capital Gain.

Proceeds minus Cost Basis: $59,940 – $40,050 = $19,890.

Step C: Determine Your Holding Period & Tax Rate.

You bought on Jan 15, 2025 and sold on Feb 20, 2026. That’s more than one year. This is a long-term capital gain.

As of 2026, long-term gains are taxed at special rates (0%, 15%, or 20%). Let’s assume you fall into the 15% bracket.

- Your Tax Owed: $19,890 x 0.15 = $2,983.50.

If you had sold after only 11 months, that $19,890 would be added to your ordinary income and taxed at a higher rate, maybe 24% or more. By holding over a year, you saved a significant amount.

Doing this for every single transaction is where it gets complex. This is why using a reputable crypto tax software that can import all your data and apply your chosen cost basis method is a huge time-saver. They handle the millions of calculations so you don’t have to.

Getting tax calculations right is a big part of confident crypto investing. For more straightforward lessons on topics like this, security, and strategy delivered in plain language, consider joining the free Clicks and Trades newsletter. It’s designed to help beginners make informed decisions without the overwhelm.

Ready to make smarter, more informed crypto decisions? Sign Up for the free Clicks and Trades newsletter to get helpful tips and guidance sent directly to you.

A Simple Table: Common Crypto Transactions & Their Tax Implications

Now that you understand the basic calculation, let’s see how it applies to different things you might do with crypto. Not every transaction creates a taxable event right away. Here’s a clear breakdown of three common scenarios.

| Transaction | How It’s Taxed | Key Tax Event |

|---|---|---|

| Buying BTC with USD | This is not a taxable event. You are simply exchanging one asset (cash) for another (crypto). | None at the time of purchase. You are establishing your cost basis for future calculations. |

| Receiving Crypto as Payment | This is treated as ordinary income. You owe tax on the fair market value of the crypto at the moment you receive it. | When you receive it. If you later sell that crypto, you’ll also owe capital gains tax on any profit from that sale price. |

| Trading ETH for SOL | This is a taxable event. Trading one crypto for another is treated as selling the first asset (ETH) and buying the second (SOL). You realize a gain or loss on the ETH. | At the time of the trade. You must calculate the gain/loss on the ETH based on its cost basis. The SOL you receive gets a new cost basis equal to its market value at the time of the trade. |

The crypto-to-crypto trade is where many people get surprised. The IRS sees it as a sale, even though you never touched dollars. This is why tracking your cost basis for every coin, as discussed in guides from experts like Koinly, is so important. Using a good crypto calculator can automate tracking these complex trades across your portfolio.

Understanding these rules helps you plan better. If you want more clear, step-by-step guides on topics like security and smart investing, the free Clicks and Trades newsletter breaks it all down in simple language.

Ready to make smarter, more informed crypto decisions? Sign Up for the free Clicks and Trades newsletter to get helpful tips and guidance sent directly to you.

Understanding Crypto Regulation: What Protects You (And What Doesn’t)

After getting a handle on your taxes, a natural next question is: who’s making sure this whole system is safe? The word "regulation" gets thrown around a lot, but what does it actually mean for you, the everyday user?

Let’s break down what current rules protect, what they don’t, and how you can stay safe.

The Role of Exchange Licensing: Your First Layer of Defense

When you use a major crypto exchange, the most important protection comes from its licenses. A license means the platform has been approved by a government authority to operate, but the requirements vary wildly.

In the U.S., a licensed exchange typically needs two main things:

- Federal Registration: They must register as a Money Services Business (MSB) with FinCEN, which involves anti-money laundering (AML) and "know your customer" (KYC) rules.

- State Licenses: They need Money Transmitter Licenses (MTLs) in each state they operate. These can be incredibly expensive, with costs ranging from $5,000 to over $150,000 per state. New York’s famous BitLicense can cost applicants up to $500,000.

States like California, Illinois, and Louisiana have now created their own comprehensive licensing rules similar to New York’s. This patchwork system is meant to ensure exchanges hold enough capital and follow strict consumer protection and security rules.

The big takeaway? A properly licensed exchange has been vetted. It is required to keep certain records, protect your data, and maintain financial reserves. Before you sign up anywhere, checking for these licenses should be part of your safety first checklist for judging a trading platform.

Custody vs. Self-Custody: Where the Protection Ends

This is the most critical line in the sand. Regulation protects the platform, not necessarily your assets once you move them.

- Custodial Protection (On an Exchange): When your crypto sits on a licensed exchange, it is held in their "custody." You are protected by their security systems and insurance policies. However, you are also trusting them completely. If the exchange is hacked or goes bankrupt, you become a creditor in line to hopefully get your funds back.

- Non-Custodial Protection (In Your Own Wallet): When you withdraw crypto to your own private wallet (like a hardware or software wallet), you move to "self-custody." This is where almost all regulatory protection stops.

You are your own bank. The rules that govern exchanges do not follow your coins into your personal wallet. This is why learning how to avoid beginner mistakes with a non-crypto wallet is a fundamental skill.

The Securities and Exchange Commission (SEC) has been pushing for stricter "qualified custody" rules for exchanges, which could change how assets are held in the future. Staying informed on these shifts is key for long-term planning, including your long term crypto tax strategy, as reporting requirements can evolve with new laws.

The Non-Negotiable Consumer Warning: Irreversible Transactions

No discussion of crypto safety is complete without this warning: Most cryptocurrency transactions are permanent and irreversible.

This isn’t a bug. It’s a core feature of the technology. But for users, it means:

- If you send crypto to the wrong wallet address, it is gone forever.

- If you are tricked by a scammer into sending payment, you cannot call your bank to reverse it.

- If you lose the password (seed phrase) to your own wallet, no customer service can recover it for you.

Regulation cannot undo a blockchain transaction. Licensing can’t get your Bitcoin back if you send it to a scammer. This puts the ultimate responsibility on you. It’s the biggest reason why a measured, learning-first approach is so vital.

The regulatory landscape is shifting fast, with major deadlines like the EU’s MiCA rules and ongoing U.S. debates like the crypto market structure bill. For a beginner, it can feel overwhelming to track.

A great way to stay updated without the stress is to follow clear, beginner-focused guidance. The free Clicks and Trades newsletter breaks down these complex topics—from safe trading practices to understanding new regulations—into simple, actionable advice.

Want to navigate crypto’s rules with more confidence? Sign Up for the free Clicks and Trades newsletter. Get the clear, step-by-step guidance you need to make smarter and safer decisions in this fast-moving space.

The Biggest Crypto Tax & Regulation Mistakes Beginners Make

Understanding the rules is one thing. Avoiding the most common pitfalls is another. Even with the best intentions, beginners often stumble into traps that can lead to big headaches, audits, or even lost funds down the line. The good news? Every single one of these mistakes is avoidable with a little bit of know-how.

Here are the three biggest crypto tax and regulation mistakes you need to steer clear of right from the start.

Mistake #1: Assuming Small Transactions Don’t Need to Be Reported

This is the most widespread misconception. You might think, "It’s just a few dollars, the IRS won’t care." But here’s the thing. In the eyes of tax authorities, every single trade, sale, or swap of cryptocurrency is a potential taxable event. The amount doesn’t matter for reporting requirements.

A 2026 survey found that only 49% of crypto users correctly identified that a taxable event occurs every time crypto is sold. This huge knowledge gap gets people into trouble. Whether you made $5 or $5,000, you need to track it.

Why is this so critical for your long term crypto tax health? Because when you finally sell an asset you’ve held for years, the government will want to know its "cost basis"—what you originally paid for it. If you haven’t been tracking all those small, early transactions, figuring out your true profit (and your correct tax bill) becomes a nightmare. This applies whether you’re dealing with crypto short term capital gains tax or long-term holdings.

The rule is simple: Track everything from day one.

Mistake #2: Using an Unregulated Offshore Exchange to ‘Avoid’ Taxes

The idea is tempting. Use an exchange based in another country with looser rules, and maybe you can fly under the radar. This is an incredibly risky strategy that can backfire spectacularly.

First, it’s important to know that tax evasion is illegal. Authorities are getting much better at tracking crypto activity across borders. Major regulatory proposals, like the ongoing debates around a U.S. crypto market structure bill, are designed to increase transparency and reporting.

Second, remember our discussion on regulation? Using an unregulated platform means you have zero consumer protection. If the exchange is hacked, freezes withdrawals, or simply disappears with your funds, you have no recourse. You’ve traded safety for a false sense of secrecy. Always start with a licensed, reputable platform as part of your safety first checklist for judging a trading platform.

Mistake #3: Not Keeping Records Because ‘The Exchange Will Have Them’

Relying solely on your exchange’s records is a classic beginner error. Yes, regulated exchanges keep records, but those records are often incomplete for your tax needs. They might not track the cost basis of crypto you transferred in from another wallet. They won’t have records of your decentralized trades or NFT purchases on other platforms.

What happens if you close your account, or the exchange changes its reporting format? Your history could become difficult to access. A separate 2026 study revealed that half of crypto investors are unaware of their full tax obligations, often because they don’t have a complete picture of their own activity.

Your responsibility is to maintain your own complete ledger. This includes:

- Dates and amounts of every buy, sell, trade, and earn.

- The wallet addresses you send to and receive from.

- The fair market value in your local currency at the time of each transaction.

This practice is non-negotiable for accurate long term crypto tax reporting. It also makes you a more secure and informed investor, helping you avoid common beginner mistakes with your assets.

Navigating taxes and rules doesn’t have to be scary. It just requires a clear, step-by-step approach. For ongoing guidance that breaks down these complex topics into simple, actionable advice, consider following the free Clicks and Trades newsletter. It’s designed to help beginners stay updated on regulations and build safe, smart habits without the overwhelm.

Ready to build your crypto knowledge on a solid foundation? Sign Up for the free Clicks and Trades newsletter. Get clear, straightforward guidance delivered to your inbox, helping you avoid these common mistakes and grow your confidence.

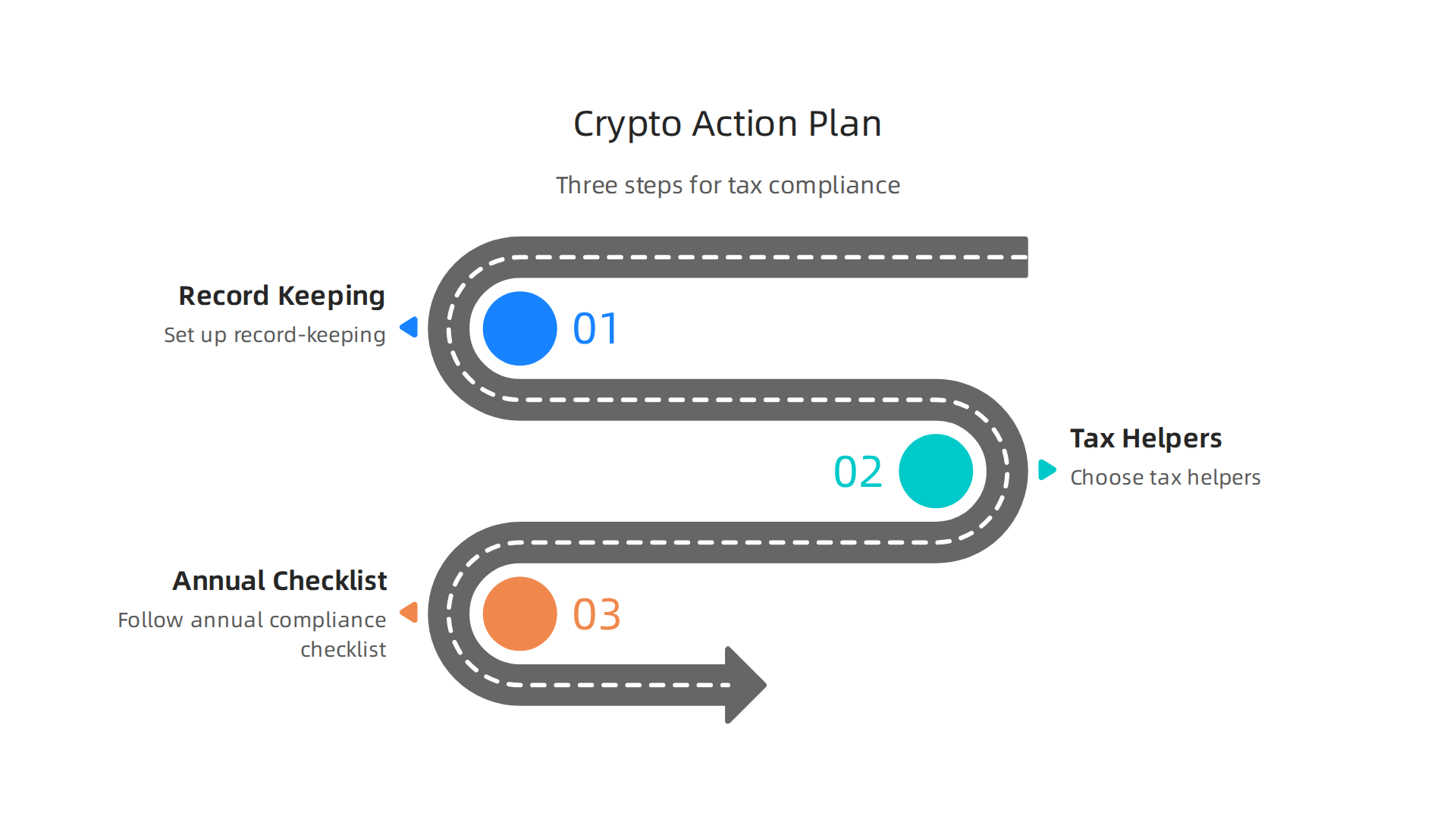

Your Action Plan: Getting Compliant and Staying Secure

Now that you know what not to do, let’s focus on what you should do. Building a solid system for your long term crypto tax health doesn’t need to be complicated. It just needs to be consistent. Think of it like brushing your teeth for your finances. A little daily effort prevents a major headache later.

Here is your simple, three-part action plan to get compliant and stay secure.

Step 1: Set Up Your Record-Keeping System (Today)

This is the most important step, and you can start right now. Your goal is to have one central place where you log every single crypto move. Don’t rely on memory or scattered exchange emails.

A basic but effective system can be a simple spreadsheet. Create columns for:

- Date of the transaction

- Type (Buy, Sell, Trade, Earned as Interest)

- Asset (e.g., Bitcoin, Ethereum)

- Amount in crypto

- Value at Time in your local currency (like USD)

- From/To (Which exchange or wallet address)

- Fees paid

If a spreadsheet feels daunting, this is where smart tools come in. Modern crypto tax software can connect directly to your exchange accounts and wallets, pulling in this data automatically. A good tool acts like a personal bookkeeper, tracking your crypto short term capital gains tax and long-term holdings without the manual work.

The point is to start. Log your next transaction. Then the one after that. This habit is your foundation.

Step 2: Choose Your Year-End Helper: Software or an Accountant

When tax season rolls around, you’ll need to turn all that data into official forms. You have two main paths.

Path A: Crypto Tax Software

For most beginners and active traders, specialized software is the easiest bridge between your activity and your tax return. The best platforms do more than just math. They connect to hundreds of exchanges, classify your transactions correctly, and generate the reports you need, like the IRS Form 8949.

When choosing software in 2026, experts suggest looking for a few key features. It should connect to all the exchanges and blockchains you use, have a clear interface, and prioritize the security of your financial data. Reading a current comparison, like this guide on the top crypto tax software programs, can help you pick the right tool for your specific needs.

Path B: A Crypto-Savvy Accountant

If your situation is complex (think high volume, lots of DeFi activity, or owning a crypto business), hiring a professional is a smart investment. A good crypto accountant does more than file paperwork. They can offer strategic advice to legally minimize your tax liability and ensure you’re ready for any audit.

Whichever path you choose, the goal is accuracy and peace of mind. Using a reliable tool or expert is part of a good safety first checklist for judging a trading platform and your overall financial health.

Step 3: Follow Your Annual Compliance Checklist

Mark your calendar for a quiet weekend each year, well before tax day, to run through this list:

- Gather Your Records: Collect all transaction data from your central log or tax software for the year.

- Reconcile: Double-check that the totals in your system match your exchange annual statements.

- Generate Reports: Use your software or provide your accountant with the data to produce your capital gains/loss report.

- File Correct Forms: Ensure your tax return includes the necessary crypto forms (like Form 8949 and Schedule D in the U.S.).

- Plan for Next Year: Note any new types of transactions you did (like staking or NFTs) and make sure your tracking system can handle them.

Following these steps transforms crypto taxes from a scary unknown into a manageable routine. It protects you from future audits and gives you a crystal-clear picture of your investment performance.

Building this knowledge takes time, but you don’t have to do it alone. For ongoing, step-by-step guidance that breaks down topics like regulations and safe investing into simple lessons, follow the free Clicks and Trades newsletter. It’s designed to help you build confidence without the overwhelm.

Ready to take the next step with clarity? Sign Up for the free Clicks and Trades newsletter. Get straightforward advice delivered to your inbox, helping you turn compliance from a chore into a strategic advantage.

Summary

This article explains why taxes and regulation are the biggest source of anxiety for new crypto users and gives clear, practical steps to convert that fear into confidence. It covers the core rule that U.S. authorities treat crypto as property, lists the common taxable events (selling, trading, spending, and earning), and shows how the one-year holding period creates a large difference between short-term and long-term tax rates. You’ll learn how to gather transaction records, calculate cost basis (including fees), and choose methods like FIFO or HIFO to manage your tax bill. The guide also explains custody risks, what regulation protects, and why keeping your own ledger matters. It highlights three frequent beginner mistakes—ignoring small transactions, using unregulated exchanges, and relying solely on exchange records—and offers a three-step action plan: record everything, pick software or an accountant, and run a yearly reconciliation. Follow these steps and you’ll be able to estimate taxes, reduce surprises, and keep your crypto holdings safer and compliant.